April to June 2022 seafood supply chain analysis: Rising prices and cost of living taking hold

Seafood supply chains are complex and shocks to the supply chain can have wide-ranging effects. We started pulling our seafood sector insight together in to a single, quarterly report during the Covid-19 pandemic. Our quarterly Covid-19 Impact Assessments helped companies and Government to understand what was going on across seafood landings, trade, processing, retail and foodservice.

We have evolved those reports to look at everything going on in the industry and what affect it has on performance.

Rising prices and cost of living are starting to bite the industry

Our latest report just published looks at what has been affecting the UK seafood industry between April and June 2022.

Prices, especially those for food, energy and fuel, continued to rise at their fastest rate for 40 years. Inflationary pressure increased operating costs for businesses across the supply chain and squeezed consumer budgets, impacting both supply and demand for seafood.

During this period, many businesses faced increased raw material, food production, energy and transportation costs but had not yet passed these cost increases on to their customers. However, it is expected that these businesses will eventually need to raise prices to keep operations viable. With these rising costs also hitting consumer finances hard, businesses were concerned about the impacts of inflationary pressures on medium term seafood demand.

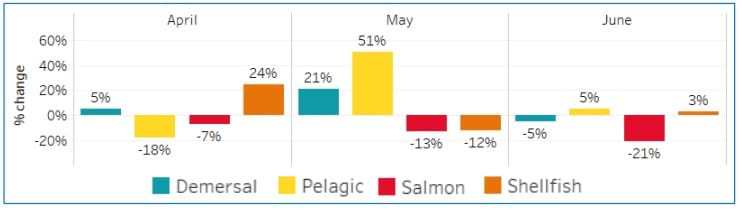

Alongside these domestic challenges, export demand for UK seafood remained strong during this period. The table below shows compared to the same period last year, export value for demersal species was up 26% in April and May, pelagic species was up 56% in May and June and shellfish was up 27% in April and June. Only salmon showed a decline in value over the period.

However, regulatory changes related to EU Exit continue to impact businesses.

Labour shortages also continued to hamper operations across the supply chain. Staff shortages in the hospitality sector led some businesses to reduce opening hours. Across the processing sector, some businesses were unable to fulfil orders and contracts due to staffing issues, causing them to lose income and customers. In the catching sector, some vessels reported sporadically tying up due to crewing issues. During this period, labour issues in the fishing fleet were also exacerbated by high fuel prices which reduced available crew share (wages).

So, what’s happened in April to June this year across each of the UK seafood sectors? We’ve summed up the key points:

Markets

- Consumers bought less meat and seafood in retail due to record inflation and historically high food prices.

- Foodservice businesses struggled with rising operating costs, but visits were up 31% compared to the same period in 2021.

- Export demand was strong with businesses feeling optimistic about markets continuing to reopen.

Production and Distribution

- Processing businesses continued to face labour shortages and difficulties in recruitment and retention, while other costs including energy and seafood raw material rose further.

- Supply chain logistics were hampered by issues at the port of Dover, rail strikes and rising fuel costs for transportation vehicles.

- Labour shortages remained a challenge across the supply chain.

Supply and Primary Production

- Even though the UK did not introduce additional tariffs on seafood imported from Russia during this period, importers still faced rising raw material costs and sourcing issues.

- Fuel costs peaked during this period, challenging some fishing businesses while others were kept afloat by high fish prices.

- The Scottish salmon sector continued to call for more immigration flexibility while shellfish farmers faced issues with water quality.

Full data and analysis are available from our PDF report and on our interactive dashboard on Tableau.

Data and analysis from January 2020 can be found in the dashboard or by searching for ‘supply chain overview’ on our website.

Share your feedback

We are always seeking ways to improve our offering to the seafood industry. Share your feedback on the dashboards and on the reports by emailing seafish@seafish.co.uk or use the feedback buttons below.